Dollars to Euros: The Cheapest Way to Actually Get Your Euros

Converting dollars to euros is simple arithmetic — divide by about 1.0834 — but whereyou do it decides whether you keep €995 or €915 of every €1,000's worth. The rate is the same for everyone; the markup is not. The worst dollar-to-euro deal you can get is usually the currency desk at the airport you just landed in, and the best is often the bank ATM 10 steps past it. This guide walks through the four ways to get euros, ranks them by real cost, and covers the small traps — flat ATM fees, declined cards, the "pay in dollars?" prompt — that quietly drain a European trip budget.

Four Ways to Turn Dollars Into Euros, Ranked by Cost

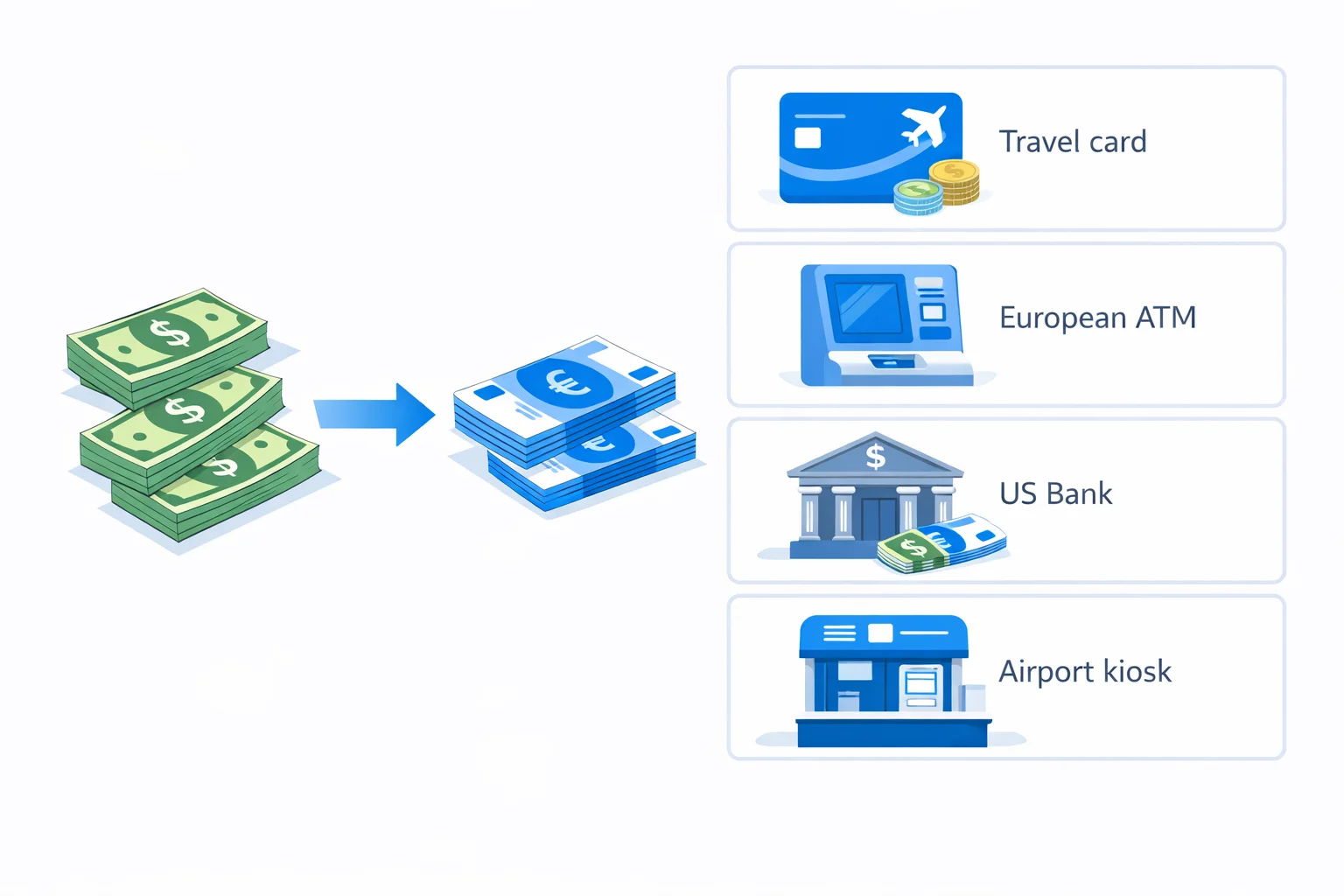

Take $1,000. At the mid-market rate of 1.0834, that's €923 of pure buying power before anyone takes a cut. Here's what four common routes actually deliver:

- No-FX travel or credit card (0%): about €923 — the mid-market rate, minus nothing, on every tap.

- European bank ATM (one €3.50 fee): about €919, roughly 0.4% — the cheapest way to hold euro cash.

- Euros ordered from a US bank (~4%): about €886, so about $37 evaporates before you leave home.

- Airport or hotel kiosk (~9%): about €840 — an €83 gap versus the card, for the same dollars on the same day.

That spread is the whole ballgame. A card and an ATM sit within a euro or two of the fair rate; a kiosk can cost you a nice dinner for two. The comparison table in the tool above runs these figures on whatever amount you type, and our multi-currency converter applies the same markup logic across 160+ currencies if your trip isn't only to the eurozone.

The €3.50 ATM Fee That's 9% One Way and 0.9% the Other

An ATM's flat fee is the sneakiest cost in travel money, because its percentage bite depends entirely on how much you pull. A €3.50 fee on a €40 withdrawal is 8.75% — kiosk territory. The exact same €3.50 on a €400 withdrawal is 0.875%. Nothing changed but the size of the pull. So the rule writes itself: take fewer, larger withdrawals. Five €80 stops cost €17.50 in fees; one €400 stop costs €3.50, a €14 saving for a single extra button press.

Two more ATM traps cost more than the fee itself. First, when the machine asks whether to charge your card "in your home currency," it's offering dynamic currency conversion — decline it and choose euros, or you hand over another 3-12%. Second, stick to bank-branded ATMs (BNP Paribas, Deutsche Bank, Santander). The standalone machines clustered in tourist zones, usually Euronet-branded, layer on a €5-10 fee plus a poor built-in rate that can top 10% combined.

Where a US Card Quietly Gets Refused

A US card works at the overwhelming majority of staffed tills in Europe — contactless and chip are everywhere. The failures cluster at unattended machines. Automated train-ticket kiosks, highway toll booths, parking meters, and overnight gas pumps often demand chip-and-PIN, and many US cards are chip-and-signature. The transaction just dies with no cashier to wave it through. That's exactly why you carry €50-100 in cash even when you plan to tap for everything.

Check one number before you fly: your card's foreign transaction fee. Plenty of everyday US cards still charge 3% on every euro purchase, which adds $90 to a $3,000 trip for nothing. A no-foreign-transaction-fee card — most travel cards and a growing list of no-annual-fee ones — charges 0% and settles at the network's mid-market rate. It's the single highest-leverage decision here, and it's free.

What $100, $500, and $2,000 Actually Come To

Every dollar-to-euro conversion is one division: dollars ÷ rate = euros. At 1.0834:

- $100 to EUR: 100 ÷ 1.0834 = €92.30.

- $500 to EUR: 500 ÷ 1.0834 = €461.51.

- $2,000 to EUR: 2,000 ÷ 1.0834 = €1,846.04.

No calculator handy? Knock about 8% off the dollar figure and you're within a rounding error, because the euro currently carries roughly an 8% premium. So $250 minus about $20 lands near €230 (the exact answer is €230.75). That trick drifts as the rate moves — at 1.10 you'd shave closer to 9%, at parity nothing at all — but it's plenty accurate to sanity-check a menu or a market stall. Pin any day's official number against the Federal Reserve's H.10 exchange-rate release, which publishes the dollar-euro rate every business day.

Pay in Euros, Every Single Time

One habit saves more than all the ATM math combined: at any European card terminal that asks "pay in EUR or USD?", choose EUR. Picking dollars triggers dynamic currency conversion, where the merchant's processor sets the rate and pockets a 3-12% markup. On a €200 purchase, a 7% DCC hit is about $15 gone — for the dubious comfort of seeing the price in dollars. Your own card issuer already converts at a far better rate, so let it. The prompt is designed to sound like a favor; it isn't.

Sending Larger Sums: Invoices, Tuition, and Property

Trip cash is one thing; wiring five or six figures to Europe is another. On a $10,000 transfer, mid-market gives you €9,230. Push it through a typical bank and you face two costs stacked together: an exchange spread of around 2% (about €185) and a flat SWIFT wire fee of $30-45. A specialist like Wise or OFX charges closer to 0.4% (about €37) with a smaller fixed fee — a difference of roughly €150-190 on one transfer. On a euro tuition bill or a property deposit, that's real money for choosing the right rail.

Two practical notes. The flat fee flips the logic on small transfers: a $40 wire fee on a €300 payment is over 13%, so for anything under a few hundred euros, a card or a low-cost app beats a bank wire outright. And once your money reaches a euro account, moving it onward within Europe is cheap and fast via the Single Euro Payments Area (SEPA), which standardizes euro transfers across 36 countries — you just need the recipient's IBAN. If the transfer is large enough that the rate itself matters more than the fee, our USD to EUR rate guide breaks down what a single cent of movement does to the total.

How Much Euro Cash Should You Carry?

For a normal trip, €100-200 in cash is plenty to land with. It covers the airport train or first taxi, a meal before your card habits kick in, small tips, and the cash-only corner café or Sunday market that never took cards anyway. Everything else rides on a no-FX card, and you top up at a bank ATM if the cash runs low.

The mistake is over-converting "to be safe." Leftover euros are hard to unwind: US banks buy euro notes back at a poor rate and take no coins at all, so €30 in loose change is effectively $0 the moment you fly home. If you do come back with a stack of notes, our euros to dollars converter shows what each buy-back method actually costs — but the cheaper move is simply not to hold more euro cash than a day or two of spending in the first place.