How Exchange Rates Work — and Why You Rarely Get the One You See

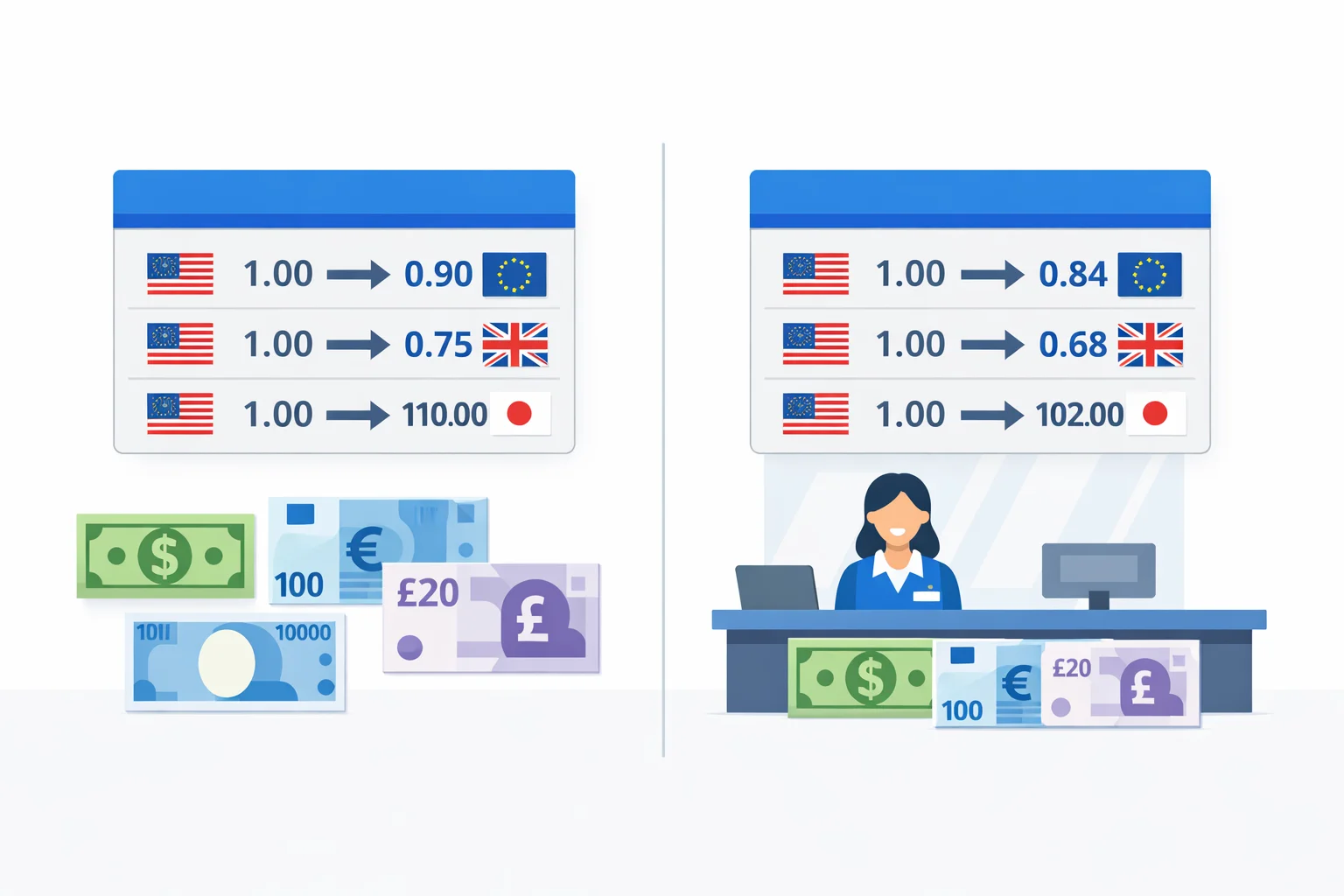

A currency converter gives you a number in under a second — but here's the catch that costs travelers and freelancers billions every year: the rate you see is almost never the rate you get. The figure above is the mid-market rate, the wholesale price banks trade at with each other. Walk into a branch or tap your card abroad and a markup gets layered on top, usually 2-4%, sometimes 15%. This guide shows you how to read the real cost of a conversion, not just the headline.

The Rate You See vs the Rate You Get

Every currency pair has two prices at any moment: a bid (what buyers will pay) and an ask (what sellers want). The mid-market rate is the exact midpoint. If euros are bid at 0.921 and asked at 0.925 per dollar, the mid-market rate is 0.923 — the number this tool and Google both show. The gap between bid and ask is the spread, and that spread, widened, is where providers make their money.

Consumer rates simply move the price away from the middle in the provider's favor. A bank quoting "no fees" on a euro purchase might hand you 0.895 instead of 0.923 — a 3% haircut hidden inside the rate itself. Toggle the markup buttons above and watch the real take-home figure drop while the mid-market number stays put. That difference is the single most important thing to understand about moving money across borders.

How Exchange Rates Are Actually Set

Most major currencies float — their value is set continuously by supply and demand across a $7.5-trillion-a-day global market. The dollar, euro, pound, and yen all move every second the market is open, driven by interest rates, inflation data, and trade flows. When the U.S. Federal Reserve raises rates, dollars typically strengthen because higher yields attract foreign capital. You can cross-check any pair against the Federal Reserve's H.10 exchange-rate release, the official U.S. reference series.

Other currencies are pegged — deliberately held at a fixed value against a stronger currency by their central bank. The mechanics differ completely. A floating currency reflects a live market; a pegged currency reflects a policy decision that can hold for decades. That is why the dirham line in the table above never budges while the lira swings daily.

Converting $1,000: Mid-Market vs a 3% Bank

Let's run a real conversion end to end. You're moving $1,000 into euros at a mid-market rate of 0.923:

- Mid-market: 1,000 × 0.923 = €923.00 — the fair value.

- Typical bank (3% markup): the rate becomes 0.923 × 0.97 = 0.8953, so 1,000 × 0.8953 = €895.30.

- The difference: €27.70 gone— even though the bank may advertise "zero commission."

Now scale it up. Send $20,000 to buy a property deposit and that same 3% becomes €554 lost on a single transfer. A specialist service charging 0.5% would cost €92 instead — a €462 saving on one payment. This is why the markup selector exists in the tool: the headline conversion is the easy part, and the spread is the part that decides how much actually arrives. For the most-searched pair, our EUR to USD converter breaks the euro-dollar rate down in the same way.

Where Conversion Is Cheapest (and Worst)

Not all providers are close. The spread you pay can vary by a factor of twenty depending on where you exchange. Here's how the common options stack up against the mid-market rate:

| Method | Typical markup | Watch out for |

|---|---|---|

| Specialist transfer (Wise, etc.) | 0.3-1% | Small flat fee on top |

| No-FX-fee credit card | 0-1% | Decline dynamic conversion |

| Debit card / ATM abroad | 1-3% | Plus a flat ATM fee |

| High-street bank wire | 2-4% | Often a $15-45 fee too |

| PayPal | 3-4% | Markup buried in the rate |

| Airport / hotel kiosk | 7-15% | The worst rate anywhere |

The pattern is consistent: the more convenient and visible the location, the wider the spread. An airport kiosk charging 12% turns your €923 into roughly €812 on that same $1,000 — €111 evaporated for the convenience of a counter past security.

Pegged Currencies That Barely Move

If you're converting to a Gulf or certain Caribbean currency, the rate you see today is almost certainly the rate next month. These currencies are locked to the dollar by their central banks:

| Currency | Pegged rate (per USD) | Pegged since |

|---|---|---|

| UAE Dirham (AED) | 3.6725 | 1997 |

| Saudi Riyal (SAR) | 3.75 | 1986 |

| Qatari Riyal (QAR) | 3.64 | 2001 |

| Hong Kong Dollar (HKD) | 7.75-7.85 band | 1983 |

The practical upshot: there's no point timing the market on a pegged pair. The mid-market rate won't improve, so your only lever is the provider markup. Shop the spread, not the date.

The Costly Mistakes Travelers Repeat

- Accepting dynamic currency conversion.When a terminal abroad asks "pay in USD or local currency?", choosing your home currency triggers DCC and a 3-12% markup. Always pick the local currency so your card network does the math.

- Confusing the rate with its inverse.If 1 USD = 0.923 EUR, then 1 EUR = 1.083 USD — not 0.923. Reading the rate the wrong direction on a €500 purchase makes you think it costs $462 when it's actually $542.

- Exchanging cash at the airport. The convenience costs 7-15%. Withdraw from a bank ATM in town instead, ideally with a card that refunds foreign fees.

- Ignoring weekend buffers. The forex market closes Friday evening to Sunday, so cards may add 0.5-1% on Saturday purchases to cover the Monday gap risk.

When This Converter Won't Match Your Receipt

A converter is a planning tool, not a price guarantee. Three situations will make the on-screen number differ from what you're charged. First, timing: floating rates move constantly, and a card transaction settles 1-3 days after you swipe, so the posted rate is the settlement-day rate, not the purchase-day one. Second, provider spread: unless you're quoted the exact mid-market rate (rare), expect the markups in the table above. Third, fixed fees: a $25 wire fee on a $200 transfer is a hidden 12.5% cost no percentage markup captures.

Use the mid-market figure as your honest baseline, apply the markup that matches your provider, and you'll know within a euro or two what you'll actually receive. When you need a single pair fast, the pounds to dollars converter and USD to INR converter give you the same markup-aware breakdown for those routes.